The U.S. Economy in Transition

Third-quarter data marked a meaningful transition in the economic landscape.

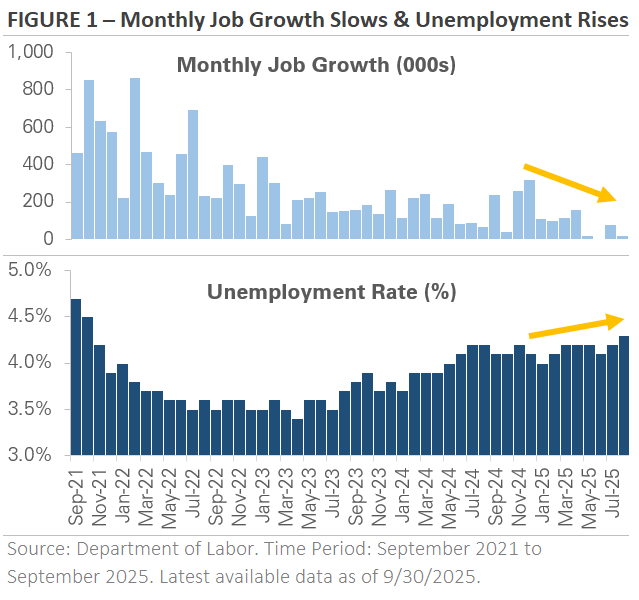

The quarter opened on solid footing. Economic activity had recovered from tariff-driven headwinds earlier in the year, and incoming data pointed to steady consumer and business demand. Job growth was healthy, consumers continued to spend, and business surveys signaled improving sentiment. The stock market advanced in July, supported by confidence that the economy could withstand relatively high interest rates and ongoing trade uncertainty without slipping into recession. By late summer, cracks began to emerge in the labor market as shown below:

Job growth slowed in May, followed by three months of weak gains in June, July, and August. The unemployment rate rose to 4.3%, its highest level since 2021. While the labor data raised concerns about a potential economic slowdown, GDP growth remained strong with inflation in check.

The shift in the economic backdrop was significant, changing the conversation around monetary policy. As the labor market softened, investors began to anticipate a more accommodative Fed, with the potential for multiple rate cuts before year-end. Slowing job growth was viewed less as a recession warning and more as a catalyst for the Fed to resume its rate-cutting cycle. The debate shifted to when—not if—the Fed would deliver its next cut.

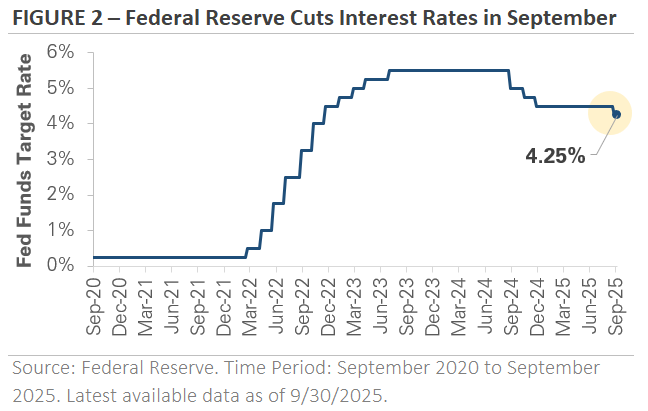

Fed Cuts Interest Rates After a 9-Month Pause

At its July meeting, the Federal Reserve held interest rates steady, citing a solid labor market and lingering inflation risk. The outlook changed just days later when the July jobs report fell short of expectations. In his late-August Jackson Hole speech, Fed Chair Powell laid the groundwork for a potential September rate cut. He noted that monetary policy remained restrictive and suggested that softening labor market data could justify a rate cut, even with inflation still above target. Powell’s remarks reinforced expectations for a September cut and signaled a shift in focus—from fighting inflation to supporting the labor market.

As expected, the Fed delivered a 0.25% rate cut in September, ending its 9-month pause as illustrated below:

Powell’s comments underscored how the current economic environment differs from past rate-cutting cycles. For example, the emergency cuts in 2008 and 2020 were in response to the global financial crisis and the pandemic, respectively. Those cycles were aimed at stimulating the economy after major shocks. By contrast, the current cycle is about fine-tuning monetary policy to help sustain ongoing economic growth.

Powell’s comments underscored how the current economic environment differs from past rate-cutting cycles. For example, the emergency cuts in 2008 and 2020 were in response to the global financial crisis and the pandemic, respectively. Those cycles were aimed at stimulating the economy after major shocks. By contrast, the current cycle is about fine-tuning monetary policy to help sustain ongoing economic growth.

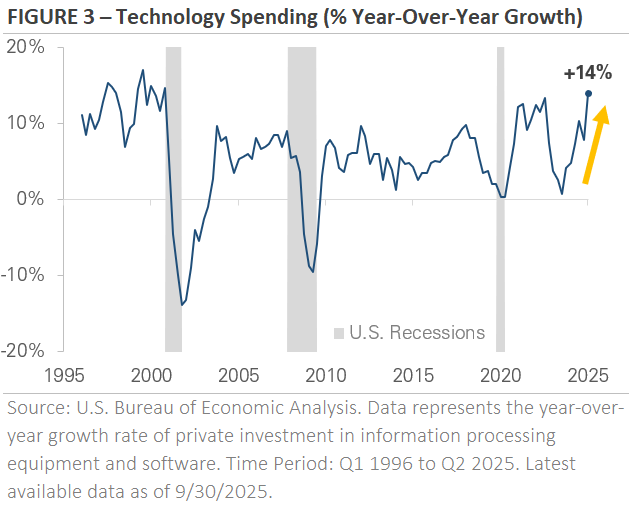

Artificial Intelligence Drives Tech Spending

Corporate technology spending grew 14% year-over-year in the second quarter—the fastest pace since the late 1990s. This acceleration is driven by the AI industry buildout, with billions flowing into high-performance chips, cloud infrastructure, data center construction, and the power and cooling required to operate them. The chart below illustrates this recent growth in tech spending:

These spending levels have become an important driver of economic growth, helping offset weakness in interest rate-sensitive sectors such as housing, manufacturing, and non-AI business investment.

AI-related spending is expected to reach hundreds of billions of dollars annually, with major cloud and infrastructure firms carrying multi-year order backlogs. Such enthusiasm explains the outsized gains in some technology and semiconductor stocks.

On the other hand, some question whether AI spending is running ahead of anticipated productivity gains and revenue growth. Even so, AI is likely to remain a key driver of corporate earnings, economic growth, and market returns for the foreseeable future.

The Final Stretch of 2025

The markets currently present a conflicting set of signals. Stocks sit near all-time highs, supported by robust corporate earnings and continued enthusiasm for technology and AI. Yet the labor market has softened, raising concerns about the underlying economy and the financial health of consumers. Valuations are historically elevated, tariff uncertainty persists, and Congress remains gridlocked. Even so, GDP growth has held up, and inflation has largely stayed in check.

Looking ahead, we remain encouraged by the resilience of the U.S. economy and the financial markets. At the same time, we are keenly aware of the challenges that remain and anticipate some degree of market volatility as economic conditions evolve. Our focus stays on what we can control—keeping your portfolio aligned with your goals and well prepared for whatever the market may bring.

If you would like additional insights or guidance, schedule a call.

-------------------

All content is for informational purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor is it intended to be a projection of current or future performance or indication of future results. Past performance is no guarantee of future results. Purchases are subject to suitability. This requires a review of an investor’s objectives, risk tolerance, and time horizons. Investing always involves risk and possible loss of capital. Opinions expressed herein are solely those of Darrell Capital Management, LLC. The information has been derived from sources believed to be reliable but is not guaranteed as to the accuracy and completeness and does not purport to be a complete analysis of the materials discussed. All information and ideas should be discussed in detail with your financial, tax and legal advisors prior to implementation. The information contained herein should be in no way be construed or interpreted as a solicitation to sell or offer to sell advisory services to any residents of any state other than the State of California or where otherwise legally permitted. Advisory services are offered by Darrell Capital Management, LLC, an Investment Advisor in the State of California. Being registered as an investment advisor does not imply a certain level of skill or training. Social post reactions and comments should not be viewed as endorsements or testimonials.